Learning basic bond terminology is crucial for all investors, whether they’re new to investing or experienced in other asset classes. It equips them with the knowledge needed to make informed, strategic, and thoughtful investment decisions in the fixed income market. This understanding of bond language allows investors to manage risks, optimize returns, and work towards achieving their financial goals.

Below are some essential bond terms that investors should be familiar with:

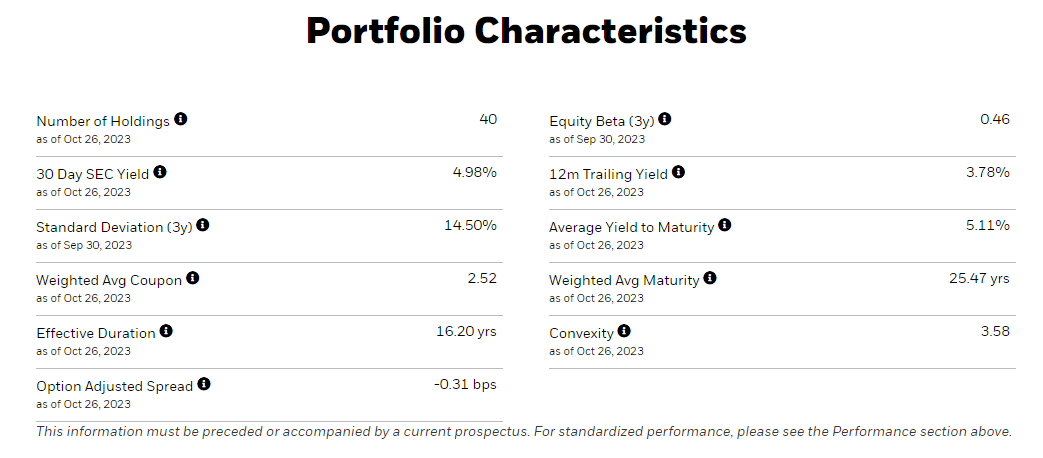

30-Day SEC Yield

The 30-Day SEC Yield, or simply the SEC Yield, is a standardized way to calculate and express the yield of a mutual fund or ETF in the United States. It’s a critical metric, especially for income-focused investments like bond funds and dividend-oriented equity funds. The SEC Yield offers a more accurate representation of a fund’s income potential compared to a simple yield based solely on the most recent distribution.

Here’s how the 30-Day SEC Yield is calculated:

1. Income Received: Calculate the income the fund earned over the past 30 days, considering interest, dividends, and other income from the underlying investments.

2. Expenses Deducted: Subtract the fund’s expenses, including management fees and other costs, from the income.

3. Net Income: The result after expenses represent the fund’s net income.

4. Average Net Assets: Determine the average net assets under management (AUM) over the past 30 days. This figure helps calculate the yield relative to the fund’s size.

5. Yield Calculation: Annualize the net income by multiplying it by a factor of 12/30 to account for a full year. Then, divide this annualized income by the average net assets to arrive at the 30-Day SEC Yield.

The 30-Day SEC Yield is expressed as an annualized percentage. It provides a more precise estimate of the income investors can expect over the next year, considering both investment income and expenses. Keep in mind that this is a historical measure, so it may not predict future performance. Additionally, the yield can fluctuate due to changes in income or expenses and shifts in the fund’s asset base.

The SEC Yield is a useful tool for comparing income-generating funds and assessing if a fund’s yield aligns with an investor’s income goals and risk tolerance. However, it should be used in conjunction with other factors like investment strategy, risk profile, and historical performance to make well-informed investment decisions.

Effective Duration

Effective Duration is a measure in finance used to assess how sensitive a fixed-income security, like a bond or bond portfolio, is to changes in interest rates. It’s a concept valuable for investors and portfolio managers in understanding how changes in interest rates affect the security’s or portfolio’s price. Effective Duration is expressed in years and helps investors estimate how much the price might change when interest rates move by 1%.

For example, if a bond or bond portfolio has an effective duration of 10 years, it means that for every 1% increase in interest rates, you can expect the bond’s or portfolio’s price to decrease by approximately 10%. If interest rates decrease by 1%, the price would increase by around 10%.

Effective Duration is a valuable tool for evaluating the risk of fixed-income investments in a changing interest rate environment. A higher effective duration implies more significant interest rate risk, making the bond’s price more sensitive to interest rate changes. Conversely, a lower effective duration indicates lower interest rate risk.

Average Yield to Maturity

Average Yield to Maturity (YTM) is a way to estimate how much you’ll earn from a group of bonds in a portfolio. It calculates the average return if you hold all the bonds until they mature. This helps you understand the potential earnings from your entire bond investment. The calculation takes into account each bond’s YTM, its price, and its weight in the portfolio.

Let’s clarify the concept of Average Yield to Maturity (YTM) with an example:

Imagine you have a bond portfolio consisting of three different bonds:

1. Bond A with a YTM of 3% and a market value of $1,000.

2. Bond B with a YTM of 4% and a market value of $1,200.

3. Bond C with a YTM of 2.5% and a market value of $800.

To calculate the Average YTM for this portfolio, you would do the following:

1. Calculate the total market value of the bonds in the portfolio: $1,000 (Bond A) + $1,200 (Bond B) + $800 (Bond C) = $3,000.

2. Calculate the total yield from each bond:

– Bond A’s yield = 3% x $1,000 = $30

– Bond B’s yield = 4% x $1,200 = $48

– Bond C’s yield = 2.5% x $800 = $20

3. Add up the total yields from all the bonds: $30 (Bond A) + $48 (Bond B) + $20 (Bond C) = $98.

4. Calculate the Average YTM by dividing the total yield ($98) by the total market value ($3,000): $98 / $3,000 ≈ 0.0327 or 3.27%.

So, the Average YTM for this bond portfolio is approximately 3.27%. This means that, on average, you can expect to earn a return of 3.27% on your entire bond portfolio if you hold all the bonds until they mature. It provides a simplified way to understand the overall return potential of the bond investments in your portfolio.

Convexity

Convexity is a measure of how a bond’s price changes in response to interest rate movements. It helps investors understand the curvature or bend in the bond’s price-yield curve. In simple terms, it shows how sensitive the bond’s price is to changes in interest rates.

For example, if you have two bonds, Bond X and Bond Y, and Bond X has higher convexity than Bond Y:

– If interest rates increase, the price of Bond X decreases, but the drop is less severe than what duration alone would predict. This means Bond X has positive convexity.

– In contrast, Bond Y has lower convexity, which means its price change is more in line with what duration predicts.

Convexity depends on several factors:

– Maturity: Longer-term bonds generally have higher convexity than shorter-term bonds.

– Coupon Rate: Lower coupon rates tend to result in higher convexity.

– Yield to Maturity (YTM): Lower YTM often leads to higher convexity.

– Embedded Options: The presence of call or put options can affect convexity.

– Credit Quality: While not a primary factor, credit quality can have some influence on convexity.

– Interest Rate Level: Convexity is not constant; it changes with interest rate shifts.

– Call Provisions: The terms of the call option impact a bond’s convexity.

– Market Conditions: Market factors and investor behavior can influence convexity.

Understanding these factors can help investors assess the interest rate risk of their bond investments more effectively. Convexity is crucial because it tells you how bond prices respond to interest rate changes, especially during significant rate fluctuations. It offers some protection to bondholders when rates rise, reducing potential price drops. Both duration and convexity should be considered when evaluating bond investments for their interest rate sensitivity.